Usance Letter of Credit

What is Usance Letter of Credit?

A usance letter of credit is a specific type of letter of credit that allows a predetermined credit period to the buyer i.e. the importer. In common business usage, a usance letter of credit is also known as a differed letter of credit.

Types of Usance Letter of Credit

Letters of credit are payment instruments used to facilitate international trade transactions. The primary purpose of a letter of credit is that it helps mitigate the risk associated with international trade for both the buyer and the seller. However, as with any payment instrument, letters of credit also have multiple secondary purposes. There are many types of letters of credit, each serving a different purpose for either the buyer i.e. importer or the seller i.e. exporter or both. One such type is the usance letter of credit.

A usance letter of credit provides a deferred payment option to the buyer. The tenor of payment is pre-decided by the buyer and the seller. The usance letter of credit can be classified into two based on their tenor. The usual tenors can be as follows:

Payment within 90 days after the bill of lading (B/L)

This means that after the B/L is issued, the buyer has a time of 90 days from the date of B/L to make the payment for the goods.

Payment within 30 days after sight

This means that on the date that the issuing bank receives the documents, from that date the buyer has 30 days to make the payment for the goods.

Let’s understand the usance letter of credit with an example –

Example of Usance Letter of Credit

Example – Mr. James (importer/ buyer) residing in the USA decides to buy goods worth USD 50,000.00 from Mr. Ravi (exporter/ seller) who is based in India. Mr. Ravi wants to use a letter of credit for payment as he wants to mitigate risk. Mr. James insists to use usance letter of credit for the transaction as he wants a credit period of 60 days to pay for the goods. Mr. Ravi agrees so Mr. James applies for a usance letter of credit of USD 50,000.00 in the name of Mr. Ravi from Bank of America. Mr. Ravi nominates Axis Bank, India as his advising bank.

Following is the sequence of the transaction –

So this the way Mr. James took the advantage of usance letter of credit and got a credit period of two months.

Usance Letter of Credit Vs. Sight Letter of Credit

Many people get confused between usance letter of credit and sight letter of credit, when in fact they are exactly opposite to each other. While in usance letter of credit there is an option of deferred payment for the buyer, in sight letter of credit the buyer has to make the payment for the goods immediately after he receives the documents. In the above example, as it was usance letter of credit Mr. James could make the payment on May 28, 2018. While in a sight letter of credit, Mr. James would have to make the payment maximum by April 17, 2018.

Advantages and Disadvantages of Usance Letter of Credit

The major advantage of usance letter of credit falls on the buyer who gets a credit period to make a payment. The buyer doesn’t get a deferred payment option in any other type of letter of credit. This means interest-free working capital for the buyer. It also results in more efficient working capital management. Furthermore, an important aspect to consider is that when using a usance letter of credit, the buyer may receive the goods even before he makes the payment. That way he gets to check the quality of goods before he makes the payment.

In contrast, the same set of advantages become disadvantages for the seller. The seller has to manage stretched out working capital as he gives a credit period to the buyer.

So the bottom line here is that a usance letter of credit is usually used when the buyer has an upper hand over the seller or if it is a buyer’s market. Due to this reason, the seller agrees to oblige to the lenient terms of a usance letter of credit.

Sanjay Bulaki Borad

Sanjay Borad is the founder & CEO of eFinanceManagement. He is passionate about keeping and making things simple and easy. Running this blog since 2009 and trying to explain «Financial Management Concepts in Layman’s Terms».

Related Posts

6 thoughts on “Usance Letter of Credit”

Needed to put you this little bit of remark to be able to thank you over again on the splendid guidelines you have documented on this page.

Yes Bhavan

(1) you can sell to your bank your receivables on LC, however the issuing bank of such LC must give their acceptance first that they will make payment in the future date, this we call it ‘bills purchased’.

(2) usually usance LC

(3) it is different, RED clause lc is allowing the Seller to receive part of the money in advance without presenting any documents to negotiating bank.

Dear sir,

If benificery bank forwrded the bill of exchange and other documents to lc issuing bank and in forwarding letter mentioned only Invoice amount istead of invoice+ Interst as per lc there is interest aftere 60 days.

Now payment received only for invoice value what to do in this case

usance letter of credit

Смотреть что такое «usance letter of credit» в других словарях:

usance letter of credit — A letter of credit payable at a determined future date after presentation of conforming documents. Bloomberg Financial Dictionary … Financial and business terms

Letter of credit — After a contract is concluded between buyer and seller, buyer s bank supplies a letter of credit to seller … Wikipedia

Letter of Credit — Ein Akkreditiv (von lat. credere, glauben, engl. letter of credit (L/C)) ist eine Bescheinigung einer Person oder Körperschaft gegenüber einer anderen. Inhaltsverzeichnis 1 Dokumenten Akkreditiv 1.1 Das Dokumenten Akkreditiv als Instrument der… … Deutsch Wikipedia

Akkreditiv — Ein Akkreditiv (von lat. credere, glauben, engl. letter of credit (L/C)) ist eine Bescheinigung einer Person oder Körperschaft gegenüber einer anderen. Inhaltsverzeichnis 1 Dokumenten Akkreditiv 1.1 Das Dokumenten Akkreditiv als Instrument der… … Deutsch Wikipedia

Dokumentenakkreditiv — Ein Akkreditiv (von lat. credere, glauben, engl. letter of credit (L/C)) ist eine Bescheinigung einer Person oder Körperschaft gegenüber einer anderen. Inhaltsverzeichnis 1 Dokumenten Akkreditiv 1.1 Das Dokumenten Akkreditiv als Instrument der… … Deutsch Wikipedia

L/C — Ein Akkreditiv (von lat. credere, glauben, engl. letter of credit (L/C)) ist eine Bescheinigung einer Person oder Körperschaft gegenüber einer anderen. Inhaltsverzeichnis 1 Dokumenten Akkreditiv 1.1 Das Dokumenten Akkreditiv als Instrument der… … Deutsch Wikipedia

Nachsichtakkreditiv — Ein Akkreditiv (von lat. credere, glauben, engl. letter of credit (L/C)) ist eine Bescheinigung einer Person oder Körperschaft gegenüber einer anderen. Inhaltsverzeichnis 1 Dokumenten Akkreditiv 1.1 Das Dokumenten Akkreditiv als Instrument der… … Deutsch Wikipedia

Risks with Outlay of Funds — Customer outstanding category. This group includes the following customer outstanding classification codes: Advances in Current Accounts Demand loans Term loans Leasing/Hire purchase facilities Discounting others Discounting banks … International financial encyclopaedia

time — The measure of duration. The word is expressive both of a precise point or terminus and of an interval between two points. A point in or space of duration at or during which some fact is alleged to have been committed. See also computation of… … Black’s law dictionary

Medici Bank — For the private bank in Austria that failed due to its investment in Bernard Madoff s Ponzi scheme, see Bank Medici. Medici Bank Industry Banking Key people Giovanni di Bicci, Cosimo de Medici, Piero di Cosimo, Lorenzo de Medici, Francesco… … Wikipedia

Usance Letters of Credit – What are they? | 2021 TFG Usance LC Guide

A Usance Letter of Credit (also known as a deferred LC) is payable at a future point following the conditions of the LC being fulfilled and the confirming documents being presented. Read our 2020 TFG Letter of Credit Guide on Usance Letters of Credit for Trade.

View all articles by Nikhil Patel

Sunday August 19, 2018

Usance (or deferred) Letters of Credit are a specific type of LC payable at a predetermined time period. When Letters of Credit were first introduced, there were a number of specific Letters of Credit that developed. This is a short guide about usance or deferred LCs.

Usance Letters of Credit (Usance or Deferred LCs)

A Usance or Deferred Letter of Credit is a term used often in trade finance. However, in order to understand a Usance Letter of Credit, it is first important to understand what a letter of credit is and why it is used.

In much international trade there is a naturally a lack of trust in cross-jurisdictional transactions, and so mechanisms are used to mitigate this risk; one being termed a letter of credit. Letters of credit are then broken down into many different types, such as at Site Letters of Credit, Usance Letters of Credit, Standby Letters of Credit and many others.

Letters of credit are used to allow the facilitation of trade between buyers and sellers of goods worldwide. In order to facilitate trade, letters of credit are put in place by the buyer and seller. By having bank issued letters of credit in place; it allows both parties to trade with comfort. Goods will be released when certain conditions have been fulfilled and correspondingly payment will be made by the purchasing bank. The issue of when payment is made; is of utmost importance when looking at different types of instruments.

Usance Letter of Credit – How does it differ?

A Usance or a Deferred Letter of Credit; is also known as a time or term LC. LC is the short-handed name for discussing a Letter of Credit. Thus, it will be a letter of credit that is payable at a predetermined or future point following the conditions in the LC being fulfilled and the confirming documents being presented.

The simplest way to understand a Usance or Deferred Letter of Credit is to compare it to a Sight Letter of Credit; this is where funds are transferred to the supplier upon the conforming documents being submitted. Where a Usance Letter of Credit is used, there is a receipt of documents by the issuing bank and where these comply with the terms of the LC, the issuing bank accepts the draft and agrees to transmit funds for payment in compliance with LC at the later maturity date. Thus, the buyer is provided with a form of credit terms; as the purchasing party will take receipt of the product purchased but have the ability to make payment at a future date.

Why is a Usance Letter of Credit used?

This financial instrument is most likely to be favoured where there is an element of trust missing between the buying and selling parties. It is important to understand what the eventual amount to be paid is set at and the interest rate on the product. The Letter of Credit will set out the time to maturity and the actual payment date; so that both parties can use this as a reference. The tenor is typically set out as being a certain amount of days following the BL date or following sight. If it is “following sight”; then this will be from the date of the documents being received by the issuing bank.

Having a usance letter of credit allows the purchaser to deploy funds into other areas of the business until payment is made.

When will a Usance Letter of Credit be used?

This financial instrument is most likely to be favoured where there is an element of trust between the buying and selling parties. It is important to understand what the eventual amount to be paid is set at and the interest rate on product. The Letter of Credit will set out the time to maturity and the actual payment date; so that both parties can use this as a reference. The tenor is typically set out as being a certain amount of days following the BL date or following sight. If it is “following sight”; then this will be from the date of the documents being received by the issuing bank.

Having a usance letter of credit allows the purchaser to deploy funds into other areas of the business until payment is made.

How does the seller have comfort?

The seller is able to trade in comfort as the payment is guaranteed by “promises” within the banking system; as the issuing bank will correspond with the advising bank and make sure that there is an understanding that there is sufficient capital or collateral buffers in order to make payment at the maturity date. Another option to the supplier is the ability to discount the Usance LC at a point, which is earlier than maturity. This will allow them an element of payment prior to the maturity date. Obviously, the creditworthiness of banks acting on behalf of the parties is of the utmost importance when using these instruments.

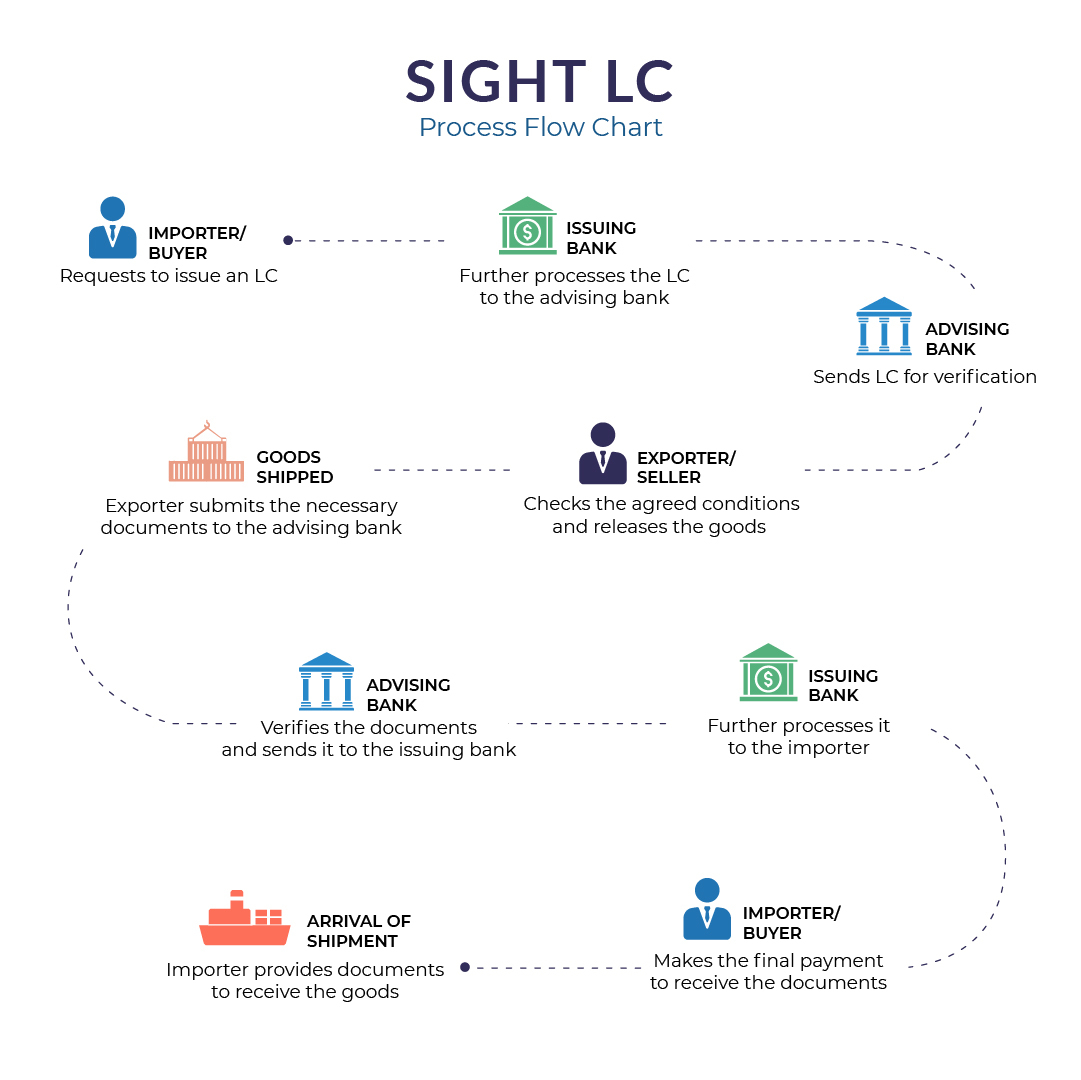

LC at Sight | Meaning & Complete process

A letter of credit (LC) is a financial document wherein banks act as an intermediary between a buyer and a seller to ensure the fulfillment of the transaction. The buyer asks his bank to issue a letter of credit to the seller or the beneficiary. The seller’s bank verifies the LC before he ships the goods. The seller ships the products and furnishes the necessary documents to the bank, upon which the bank pays the seller the full amount mentioned in LC.

There is a significant gap between the seller furnishing the documents to the bank and the bank processing the payment. This is because these documents are sent to the buyer’s bank and verified again. The buyer pays his bank within a grace period of 30, 60, or 90 days, based on the terms and conditions mentioned in the LC.

As the seller has to wait for 30-90 days to receive its payment, such transactions increase the risk for the business. However, with the help of LC at sight or Sight LC, he can avoid the payment default risk.

What is the meaning of LC at sight?

A sight letter of credit is a document which stands as a proof of payment in return of the goods or services to be released for the transportation by the seller. Once the goods or services reach the buyer, the buyer has to pay the financial institution that provided the Sight LC.

How does a Sight LC work?

Here is a step by step process of how sight letter of credit works:

A buyer who needs certain goods contacts a supplier and gets a quote for the requirement, and confirms the deal.

The buyer then goes to his bank, generally, one that has already extended him a line of credit, and asks the bank to issue a sight LC towards the supplier.

After having looked at the creditworthiness of the buyer, the bank issues a sight LC and sends it to a bank in the supplier’s country.

The supplier’s bank then informs the buyer and sends them the LC along with all the terms and conditions of the trade.

Once the supplier is happy with the LC, he ships the products and submits the shipping documents to the supplier’s bank.

The bank processes the documents and sends them to the buyer’s bank.

The buyer is alerted by the bank that the documents have arrived, and he needs to make the full payment to collect the documents. The buyer will need these documents to get the delivery of the product.

The buyer inspects the documents and pays for the LC, after which the buyer’s bank sends the payment to the seller’s bank. The seller is paid for the amount, generally much before the goods reach the buyer.

When a bank issues a sight LC, it acts as a guarantor of payment to the beneficiary. The seller has to furnish all the shipping documents mentioned under the terms and conditions in the LC to receive the payment. Once you submit all the documents and the issuing bank verifies the same, the bank releases the funds. The buyer immediately makes the full payment to the bank upon the receipt of documents.

In case the supplier is not able to provide the documents, the bank is not liable to release the payment. Furthermore, if there are any discrepancies found in the paperwork, the issuing bank can deduct a small fine from the total payment.

In the case of Usance LCs, also known as deferred payment LCs, the buyer is given a grace period of 30, 60, 90, or 120 days after receiving the documents to make the payment. This is known as LC 30 days, LC 60 days, LC 90 days, and LC 120 days.

Difference between Sight LC and Usance LC

A usance letter of credit is a type of LC wherein the buyer is allowed to make the payment after the delivery, within a stipulated grace period. Unlike with sight LCs, the buyer doesn’t have to make payment immediately to receive the documents. Usance LCs generally provide a buffer of 30, 60, 90, or 120 days to make the payment. A usance LC is also known as a deferred payment LC, or a term LC.

A Usance or a Deferred Letter of Credit; means that even after the buyer has received the goods or services the buyer gets a grace period to do the payment to the financial institution or the bank i.e 30, 60, 90 or more days as per agreed during the process.

An Example explaining Sight LC

A cold drink company called A in the US wants to buy one million bottles for their product. They identify a manufacturing company B in Singapore and contact them with their requirements. The manufacturer gives them the total cost and upon agreement, asks the buyer to make an advance payment as security before beginning production. However, the buyer does not want to take the risk of paying in advance and then not receiving the goods.

The buyer’s bank issues the sight LC and sends it to the supplier bank in Singapore. Then the bank sends the LC to the supplier, who further examines the document and starts the production process. Once the production is complete, the supplier ships it and submits the shipping documents like the bill of lading and packing bill to the bank in Singapore for examination. The bank checks the documents for any discrepancies and forwards them to the buyer’s bank in the US.

The buyer’s bank checks the documents, and once they are satisfied, it asks the buyer to pay the LC amount at sight to collect the document. Since the bank has issued a sight LC, the buyer, i.e. company A, cannot collect the documents without paying the LC amount upfront. Without it, the buyer cannot receive the goods shipped by the supplier. Once the buyer pays the amount and collects the documents, the bank sends the money to the nominated bank in Singapore. The bank in Singapore eventually transfers the money to the beneficiary.

FAQs on Sight LC

1. What is LC margin?

When a bank issues an LC, it asks for collateral that is worth some fraction of the actual LC amount. This percentage is known as LC margin.

2. Is LC at sight safe?

A sight LC is one of the safest modes of transactions as the issuing bank and the confirming bank both act as a guarantor to honor the agreement.

3. How are the LC opening charges calculated?

Opening charges are generally 0.125% of the total value of the LC. They are levied from the date of issuance until the LC expires or is paid for.

4. Can sight LC be discounted?

Sight letters of credit should not require any discount mechanism as issuing banks or confirming banks must honor at sight credits as soon as they determine that the beneficiary’s presentation is complying.

5. What is the maturity date for Sight LC?

Sight LC matures on the date on which the documents are submitted to the bank by the beneficiary.

6. Can sight LC be negotiated?

Yes, both- sight, as well as usance LCs, can be negotiated.

7. What is the limit of LC at sight?

Sight LCs are cleared by the bank within 5 to 10 working days.

8. Can sight LC be confirmed?

Sight LCs are confirmed both by the issuing bank (buyer’s bank) and confirming bank (seller’s bank). Both the banks have to honour or negotiate the LC, once they receive the documents.

LC at Sight: быстрая оплата по аккредитиву

Содержание:

Аккредитивы

Аккредитивы, включая аккредитивы до востребования, основываются на документации. Чтобы получить оплату, бенефициар (часто экспортер или поставщик услуг) должен подать документы в определенные банки. Эти документы обычно включают сам аккредитив, а также дополнительные документы, подтверждающие, что экспортер выполнил свои обязательства перед покупателем.

Если вы что-то продаете (например, покупателю за границей), вы можете обрести уверенность, используя аккредитив. При правильно оформленном соглашении вам будут платить, если вы отправите товар в соответствии с договоренностью.

Хорошо зарекомендовавший себя банк часто гарантирует оплату, поэтому вы не полагаетесь на кредит (или сотрудничество) покупателя, с которым вы не знакомы.

Если вы что-то покупаете, аккредитив поможет вам избежать оплаты того, что никогда не приходит. Вместо того, чтобы отправлять деньги и надеяться на лучшее, ваши средства хранятся на условном депонировании до тех пор, пока продавец не представит документы, подтверждающие, что он отправил вам товары или выполнил задание. Например, продавцу может потребоваться предоставить коносамент и другие документы.

Тем не менее, вы не можете исключить риск, используя аккредитив. Продавец потенциально может отправить некачественный товар или даже совершить мошенничество и отправить ящик камней. Тем не менее, вы можете снизить риск с помощью аккредитивов. Банки будут выпускать средства, если они получат документы, перечисленные в аккредитиве, вовремя и в хорошем состоянии. Банк будет нет убедиться, что грузоотправитель выполнил заказ в точности, как указано в договоре купли-продажи.

Однако вы можете потребовать сертификат проверки для аккредитива, позволяющий кому-либо проверить содержимое посылки до того, как ваш платеж будет произведен.

Что означает «немедленно»?

Хотя оплата с помощью аккредитива прицеливания происходит относительно быстро, это не обязательно мгновенно. Банк продавца (который может выступать в роли ведущего или авизующего банка) должен проверить предоставленные вами документы и убедиться, что они соответствуют требованиям, указанным в аккредитиве. Этот процесс может занять несколько рабочих дней.

В некоторых случаях документы необходимо отправить на рассмотрение в другой банк. После того, как каждый банк проверяет соблюдение требований, происходит оплата, но не стоит ожидать, что все это произойдет за один день. Наконец, хотя банковские переводы являются быстрой формой платежа, может пройти один или два дня, прежде чем средства окажутся на счете получателя (особенно, если перевод поступает из-за границы).

Вероятно, разумно ожидать, что каждый банк проверит документацию в течение пяти рабочих дней, а средства прибудут в пункт назначения еще 1-2 рабочих дня.

Альтернативные аккредитивы

Понимание того, как работает аккредитив, может помочь понять, как это работает. не Работа. Альтернативной формой аккредитива является аккредитив с отсрочкой платежа или usance (или «срочный») аккредитив.

С помощью этих инструментов оплата происходит в какой-то момент времени в будущем, возможно, спустя много времени после того, как документы были отправлены (возможно, через 30, 90 или 180 дней после).

Отсрочка платежа дает покупателю больше времени для сбора средств. В результате такой подход может работать как форма финансирования со стороны продавца. Эта стратегия может даже привлечь покупателей, которым в противном случае пришлось бы платить быстрее (но которые предпочли бы этого не делать). У покупателя также есть шанс продать импортированные товары и получить доход до наступления срока платежа, что упрощает финансирование платежа (или сокращает время, в течение которого покупатель должен занять у банка).

Аккредитивы могут иметь множество функций. Например, безотзывные аккредитивы труднее аннулировать в одностороннем порядке. Подтвержденные аккредитивы добавляют еще большую безопасность, поскольку банк, которому доверяют обе стороны, может гарантировать платеж. Такой подход обеспечивает большую уверенность, чем просто использование неизвестного банка в стране покупателя.

Зачем использовать Sight LC?

Аккредитив с оплатой по предъявлении выгоден для продавцов. Платеж поступает быстрее, чем при использовании аккредитива с отсрочкой платежа. Экспортеры тратят деньги на производство и отгрузку товаров, поэтому быстрое возвращение средств помогает им избежать дефицита денежных средств.

Быстрая оплата также предпочтительна, если у вас есть опасения по поводу платежеспособности вашего покупателя или любого из участвующих банков.

Кроме того, если вы имеете дело с покупателем (и банком) в нестабильной стране, вы можете предпочесть получать деньги как можно быстрее. Политические волнения могут привести к финансовым потрясениям, что приведет к изменениям валют, конфискации активов и другим последствиям, которые могут повлиять на платежеспособность вашего покупателя (и любых связанных банков).